🌿 Friday's Climate Infra Brief : Two Roads to a MW of Compute

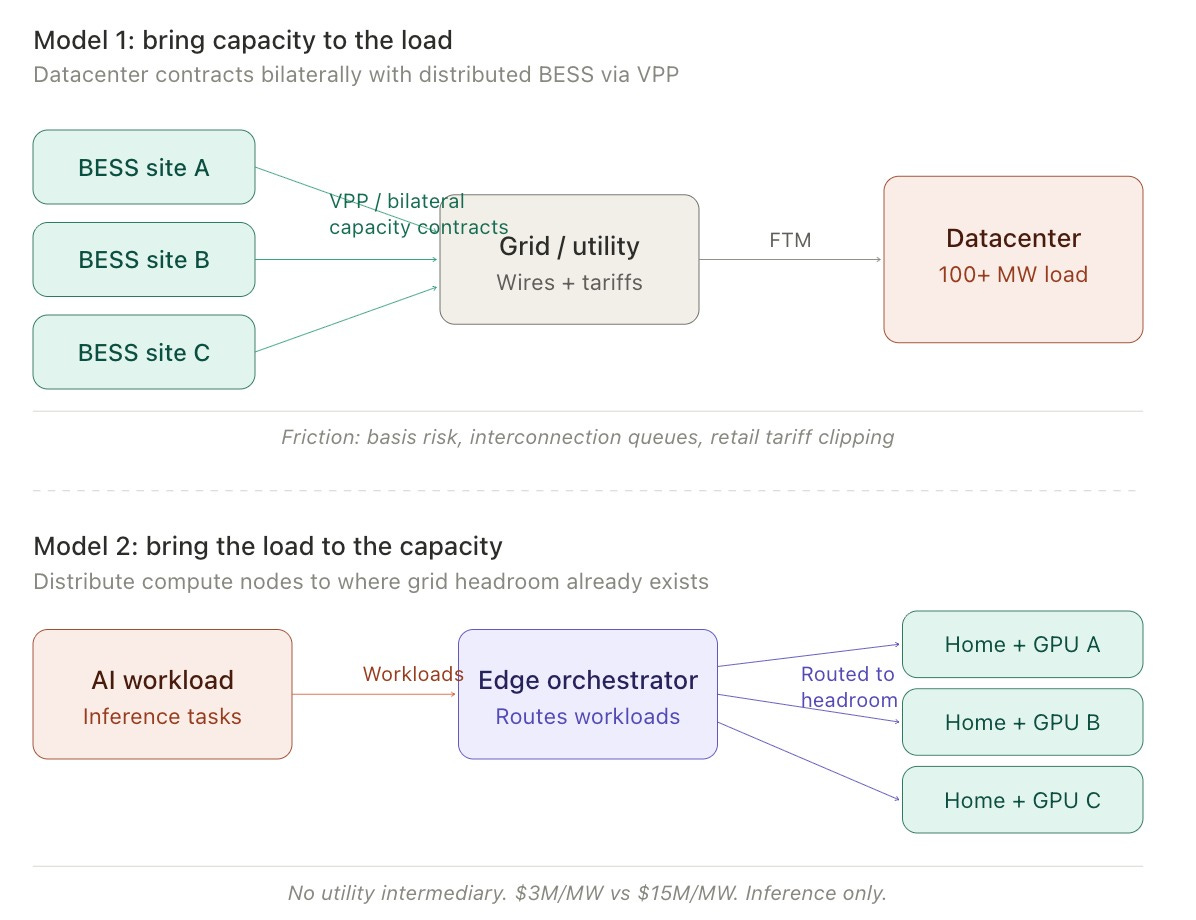

Can a large centralized load contract with distributed BESS to bring capacity to itself? Or, alternatively, can a large centralized load distributes its load to where the capacity already is?

Converting MWh into token is the most profitable energy business that everyone wants to be in right now. Nearly 2,300 GW of generation and storage capacity are sitting in U.S. interconnection queues, more than the country’s entire installed power base?! Building a 100 MW data center the traditional way takes 3–5 years. The AI buildout doesn’t have 3-5 years. Two different theories are emerging to solve the same puzzle from the opposite directions, and each implies a different view on where value sits in the AI x energy stack.

**Model 1: Bring Distributed Capacity to the Load.** Hyperscalers are starting to contract bilaterally with distributed BESS projects via VPPs or capacity agreements, sidestepping the utility as commercial intermediary. A data center stuck in PJM’s interconnection queue contracts with a portfolio of distributed 4-hour batteries to demonstrate load flexibility and shave peak demand, (hopefully) earning a faster grid connection.

Aligned Data Centers signed with Calibrant Energy for 31 MW / 62 MWh of onsite BESS at a Pacific Northwest campus, sized to accelerate interconnection “years earlier than traditional utility upgrades.” Jefferies estimates hyperscalers represent a 20 GW BESS opportunity through 2035. Wood Mackenzie reports data center demand drove a 33% jump in VPP deployments in 2025, with PJM and ERCOT leading adoption.

The structural frictions are real. You need firmness between the BESS node and the load node. Basis risk (power price difference) between nodes means a battery portfolio in West Texas doesn’t necessarily deliver firm capacity to a data center in Dallas. PJM’s ELCC framework assigns roughly 50% capacity credit to 4-hour storage; you need twice the nameplate to match a gas peaker. ERCOT has no capacity market at all, compensating storage purely through energy and ancillary revenues. CAISO’s resource adequacy rules are tighter but the market is saturated with 14 GW of operational batteries.

Then there’s FERC Order 2222, the 2020 rule meant to open wholesale markets to aggregated DERs. Six years later, implementation is glacial. NYISO targets full compliance by end of 2026; PJM and MISO filings are still under review. Retail tariff demand charges and standby rates add another friction, penalizing the exact load flexibility these contracts require.

This model seems to work, but it’s a sophisticated financial and regulatory arbitrage. The winners will structure bilateral capacity products across ISO seams and manage basis risk through a patchwork of rules. I bet some capable financiers and energy trading desks have figured this out with AI’s assistance.

**Model 2: Distribute the Compute Load to the Capacity.** SPAN announced XFRA yesterday at Latitude Media’s Transition-AI conference: a distributed edge compute system that embeds inference GPU nodes directly into homes. The premise, per SPAN CEO Arch Rao, is that the U.S. distribution grid operates at only 40–45% utilization on average, leaving substantial headroom. Each XFRA Node pairs with SPAN’s smart panel and a whole-home battery; an orchestration layer routes AI workloads across nodes based on available energy and latency. This is fascinating. Can you productize edge compute systems to be DTC shippable?

One hundred Pulte homes (third-largest U.S. homebuilder), 1,600 direct liquid-cooled inference GPUs, 1.25 MW of aggregate compute, deployable in six months. SPAN claims a cost of $3 million per MW versus $15 million for a traditional data center, though that comparison likely favors SPAN: the $15M figure covers a fully built hyperscale facility, while the $3M figure’s treatment of smart panel installation, liquid cooling infrastructure (a non-trivial engineering problem in residential settings, where heat rejection and plumbing maintenance aren’t solved at scale), and whole-home battery costs isn’t clear. Homeowners pay $150/month covering energy and internet; SPAN sells compute (inference-only) to hyperscalers and AI companies. The model sounds like third-party-owned residential solar and batteries, though deploying GPU nodes with coolant loops are a different animal than rooftop panels.

SPAN has been working on this theory for a while. They closed a $163M Series C as of February. PG&E’s SAVE VPP pilot last summer, where SPAN coordinated 400 smart panels and 1,500 Sunrun batteries for localized grid relief.

XFRA is inference-only; you can’t train frontier models across thousands of residential nodes with variable power and latency. Unit economics need new construction, which caps near-term TAM at tens of thousands of homes annually rather than millions. The orchestration challenge of delivering consistent latency across a residential network subject to homeowner behavior and local outages is a hard software problem. Hyperscaler inference SLAs are typically 99.9–99.99%; how close a residential network gets to that is the central question.

There’s also a competitive set. Purpose-built edge micro-data centers from Vapor IO, EdgeConnex, and Compass Edge already offer low-latency inference closer to end users, with commercial-grade power and cooling. The question isn’t just “centralized vs. distributed.” It’s whether inference will fragment to residential nodes further or to commercial edge colo, and hyperscalers already have bilateral deals with the latter.

---

## Where Capital Deploys

These models aren’t competing head-to-head. They solve different parts of the problem, and they imply different capital allocation strategies.

**”Bring capacity to load”** is an institutional play: BESS developers, energy trading platforms, and infrastructure credit funds that can originate bilateral capacity agreements and manage basis risk across ISO seams. The risk is regulatory fragmentation. This is fundamentally a financial engineering problem.

**”Bring load to capacity”** is potentially venture-backable. SPAN’s XFRA is a bet that AI inference will commoditize fast enough that enterprise reliability requirements relax before residential orchestration matures, and that the projected $5T+ in data center capex is structurally exposed to a low-cost distributed alternative. That’s a bold thesis. If it’s right, it creates a new asset class: distributed compute financed like residential solar, operated like a VPP, monetized through inference revenue.

The portfolio question is where along the centralization-distribution spectrum each workload class lands. Training stays centralized. Inference is up for grabs, and the capital structures will follow whoever proves they can deliver reliable compute at the lowest cost per token.

---

## Sources

- Latitude Media, “Span to launch mini AI data centers for distributed edge compute,” April 13, 2026

- Latitude Media, “Span is raising a $176 million Series C,” February 2, 2026

- Latitude Media, “Data centers are beginning to embrace batteries for onsite power,” November 3, 2025

- Latitude Media, “PG&E is testing ‘precision grid surgery’ with this summer’s VPP pilot,” September 19, 2025

- Utility Dive, “In 2026, virtual power plants must scale or risk being left behind,” January 27, 2026

- Jefferies, hyperscaler BESS opportunity estimate (November 2025)

- Wood Mackenzie, VPP market data and data center demand growth (September 2025)

- Advanced Energy United, “What ELCC is Telling Us About PJM’s Capacity Crunch,” March 2026

- Ascend Analytics, “Storage’s Moment: Capacity Markets in Transition,” October 2025

- S&P Global, ERCOT surpasses CAISO in battery storage capacity (September 2025)

- Lawrence Berkeley National Lab, “Queued Up” interconnection data (end-2024)

- FERC Order 2222 Explainer, ferc.gov

- PG&E SAVE Virtual Power Plant Program launch (March 2025)

- Aligned Data Centers / Calibrant Energy BESS deal (October 2025)

- Reuters Breakingviews, “AI dreams crash into stark $7 trln reality,” April 2026

- Sightline Climate, data center delay forecast (2026)

---

*Friday Morning Labs covers climate infrastructure, energy transition, and the capital markets connecting them.*