🌿 Friday's Climate Infra Brief - The Shape of Capital

I get asked this a lot by founders: what exactly is a structured capital solution? And most founders reasonably carry a two-option mental model for capital raising. You either raise equity, go big or go home, sell a slice of your life’s work, or you take out a loan.

But raising capital isn’t necessarily a binary. It is a spectrum. The instruments along it are really just different shapes, different ways of slicing up risk and reward, and the right shape depends on what you are actually building and financing. Funding a science experiment is fundamentally different than funding the 100th copy of a machine you already know how to make and it works, and you shouldn’t finance them with the same instrument. Once you see the full spectrum, structured capital is about picking the shape that fits.

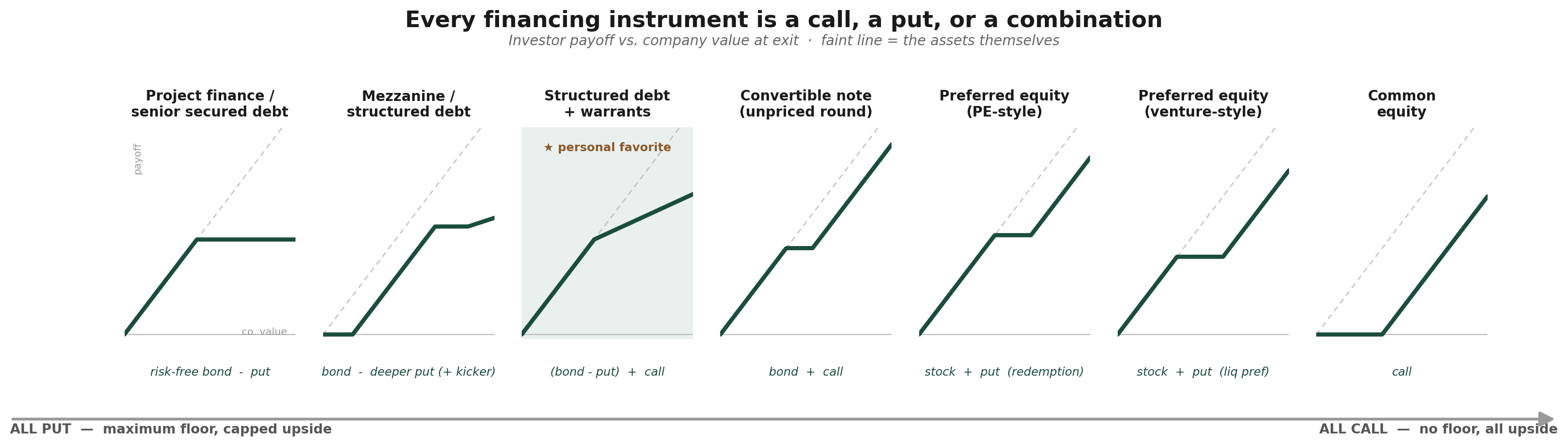

Think financial instrument as a Lego set, there are only two building blocks: a call and a put. Owning equity is a call. You get the right to everything above what the company owes, and if the whole thing goes to zero, you walk away. That walk-away right through a LLC entity is a put you hold. Lending is the exact mirror image. A loan is a risk-free bond minus a put. A lender has effectively sold the founder downside protection, agreeing to take the company assets at a floor price if things go wrong. A floor is a put. A slice of upside is a call. Most deals on earth are just some combination of those two, with the strikes and portions of the reward negotiated to parties’ taste.

It took me a while to understand why “getting a loan is long a put”. A put is the right to sell something at a fixed price, no matter how far its value has actually crashed. Now think about what a borrower gets to do. Say you lend a company $100. If the business thrives, it repays your $100 plus interest and keeps all the upside. You get none of it. But if the business collapses and the assets are only worth $50, the borrower defaults, hands you the wreckage, and walks away. They have effectively sold you the company for $100 when it’s only worth $30. That right is a put. The founder bought it. The lender wrote it. The interest on the loan is the premium the lender charges for standing behind that obligation. This is exactly why riskier borrowers pay higher rates. The put they hold is worth more, so it costs more.

And because with those two building blocks, you can stack calls and puts at different strikes, sizes, and seniorities to manufacture almost any payoff you want. For illustration purposes, a handful of the shapes that come up often.

On the far left sits the flattest shape of all: project finance. This is how most of the actual clean energy build out gets funded. It is non-recourse, secured against a single or a portfolio of bankable assets, and it’s usually cheap because the put you wrote on a contracted, operating asset is expected to be so far out of the money. Senior secured debt keep that capped, flat profile but with recourse to the whole company. Mezzanine debt sits more junior. It takes on a deeper put, charges a higher coupon, sometimes grabs a small equity kicker, and the payoff line begins to bend slightly upward at the top.

Then you reach the middle of the spectrum. This is where I spend a lot of my time. Structured debt with warrants is, in options terms, a bond minus a put plus a tiny call. You get a secured floor that protects the capital, and a warrant that lets you participate if the company takes off. The shape looks like a protected call. This shape exists because a very specific kind of company exists, with assets that are near bankable. They are deeply in money to be priced like a naked call, but not boring enough for the flat project-finance shape on the left. Think of a geothermal developer with validated reservoir but more wells still being drilled. An industrial-heat company with units running beautifully at 1-2 sites, staring down a contracted pipeline 10x larger that it can’t fund off its balance sheet. A modular water-treatment business that works perfectly but can’t finance the next 10 installs. A distributed-battery operator that needs hardware running in thousands of homes before the cash flows truly compound. The combo instrument fits them beautifully because it prices the proven part like debt and the unproven, rapidly scaling-up deployment part, like a small call.

Right around here you meet the convertible, the classic way to raise an unpriced round. The whole trick of a convertible note (or a SAFE) is that you take the money now and do not have to argue about valuation today; it converts into equity at the next priced round, when there’s more information and a lead to set the number. In options terms it’s still a floor plus a call — you’re a creditor until conversion, then you convert into the upside.

Keep going right, preferred equity, and we need to pause, because “preferred” is not one thing. It spans most of the spectrum. PE-style structured preferred often has a redemption right, a contractual obligation for the company to buy the shares back, and has a coupon that accretes the redemption value over time. That’s an engineered floor, often against a business with real cash flows, which is why it leans toward the debt end. Venture-style preferred has only a 1x liquidation preference: a priority claim on whatever exit proceeds exist, junior to every dollar of debt and senior to common. It protects you in a soft landing, where the company sells for less than its price but more than zero and you get your money back before the founders get theirs. It is worth nothing in the outcome that actually dominates venture, when the company goes to 0, 1x of 0 is 0.

At the very end of the line sits common equity: a naked call. All upside with no floor, permanent and fully dilutive. The most expensive shape there is.

AI has bent the entire market toward that right side. Capital is flooding toward companies that serve it. But a naked call is a bad shape a near-bankable company can sell. It gives away for free the floor those companies have already earned by building real assets and signing real contracts. So when a founder asks me what structured capital is, the honest answer is how much of the floor you’ve already earned, and we can go design a shape from there. And for a company that has built real things and building more, the right shape may not live at either edge.