🌿 Friday's Climate Infra Brief: How Do We Stack?

This week is a nerdier but essential piece of my quest to answer “can we make data centers more sustainable?”. You can build solar really cheap, really fast on-site, but it’s completely useless at 9pm. So, how much storage, and what tech, do you need before that power actually counts as firm?

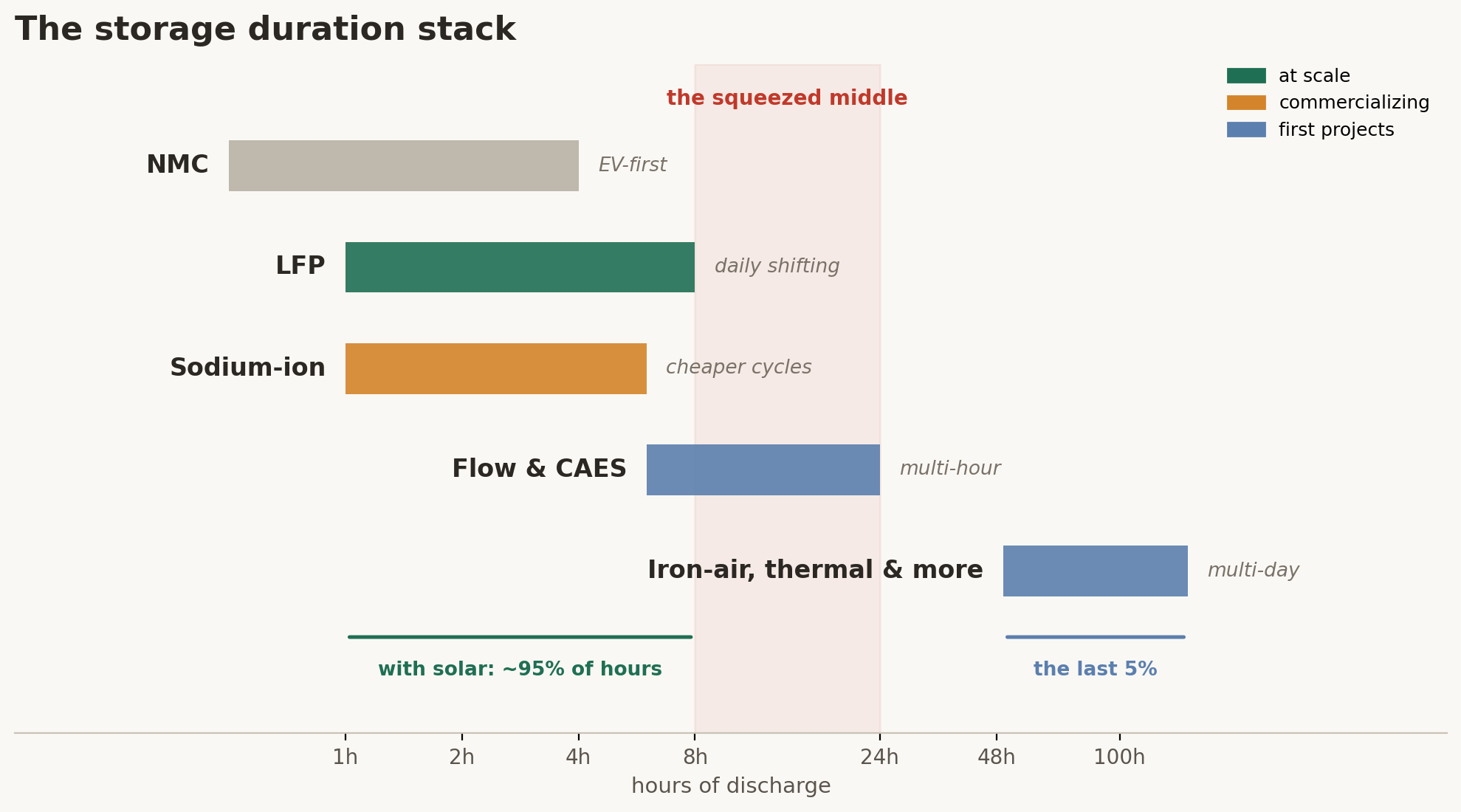

Storage tech is a stack, sorted by hours of discharge and maybe costs. Every layer has a different job. I’ll argue the case: the last 5% is where the money will be made. Let me explain.

For the bottom layer, daily shifting to move noon solar into the evening and overnight, LFP has basically won the whole board. It took about 95% of utility-scale battery awards in 2024 and 2025. Cells are trading at $55–75/kWh right now, and the EIA is projecting 24 GW of US additions just this year. I still get pitched NMC batteries for grid projects occasionally, which makes zero sense to me. Yes, NMC built the EV industry. Its whole edge is energy density. If you’re trying to cram capacity into an EV chassis where weight and space are binding constraints, great. But a grid battery is literally just a container sitting on a lot discharging over 4 hours. Density buys you nothing. All you get is the massive cobalt bill, half the cycle life, and a fire record (we all remember Moss Landing was NMC).

There is a new entrant at the daily layer: sodium-ion. It competes purely on cost per cycle, using incredibly cheap, abundant materials and boasting 15,000+ cycle claims. The smartest thing CATL did was build their new sodium cell on their existing lithium platform so integrators can swap it in without retooling lines. Makes that 60 GWh sodium order they booked in April look very real. Peak Energy shipped the first US grid-scale sodium systems last year. GM stepping in as a cell partner with them is a great signal.

If you stack solar with 4-8 hours of this stuff, you get close to firm power. A Berkeley team ran 8 years of hourly weather data across 68 sites and found that solar-plus-storage covers over 95% of a data center’s demand at $60–138/MWh. IRENA is putting firm solar-plus-storage at $54–82/MWh in sunny locations. That outright beats new gas, but you take on the long tail of weather risk. I know the prevailing argument in the market is data centers/AI factories are cost insensitive, but over time, the marginal cost of AI might be closer to the marginal cost of electricity.

Now let’s talk about the last 5%: the three-day cloudy stretch; extreme weather events, you can’t just oversize daily batteries to cover that; the capex gets absurd. This is where multi-day storage comes in, and the economics completely invert. Because the asset sits idle most of the year, round-trip efficiency barely matters. Raw cost per kWh of capacity is the only metric you care about. Form Energy’s iron-air battery is intentionally slow and inefficient, targeting $20/kWh with 100 hours of discharge. Google buying that first big project—300 MW / 30 GWh for a Minnesota data center, paired with 1.6 GW of new wind and solar—is huge. It’s the first time anyone has actually bought that last 5% as a standalone product instead of just giving up and throwing in a gas turbine.

I still haven’t figured out the squeezed middle. The 8–24 hour technologies like flow batteries and compressed air. The job is real (bridging a single bad day), but LFP keeps getting cheap enough that developers just buy more hours of lithium, and the 100-hour guys are potentially locking up the multi-day bids. The US players stuck in the middle are bleeding out.

China’s dynamic is intriguing right now. They’ve de-risked nearly every component of this stack, but they aren’t assembling the stack for a reason. Cumulative storage hit 144.7 GW by the end of 2025, up 85% in a single year. They have flow and compressed-air plants at hundred-MW scale operating, not just piloting. The Baochi station in Yunnan, the world’s first grid-forming sodium-ion plant at 200 MW / 400 MWh, went up in 7 months. Seven months! But it’s all grid-side, firming wind and solar farms. Chinese data centers don’t firm on-site because they don’t have to: their grid is strong, interconnection isn’t the bottleneck, and they meet the 80% green-power rule mostly through grid purchases and siting near renewable bases. The national compute-power coordination policy push trying to turn data centers into flexible, dispatchable loads, is still mostly aspirational. Nobody has figured out how to map compute tasks to power load precisely enough to dispatch against it yet. So we have this fun split: China de-risks the hardware, and the US actually pieces the complex systems together under duress, purely because our grid failed the load.

Can stacking storage tech make solar firm? Mostly, and cheaply. The daily layer gets you 95% of the way there. For the last 5%, there are really only three sellers: gas (tracking 101 GW of behind-the-meter announcements right now, and Bloom’s stock went up by 1000% YoY, a 10x that everyday people could actually access), 100-hour storage (just the one Google order so far), or the grid itself.

The grid is the ultimate top layer of the stack, infinite duration, deepest firmness. But it’s honestly a deeply underpriced insurance product. Because it’s egalitarian by design, utilities recover costs at a fixed, regulated margin spread across everyone. A self-supplied load draws on it exactly when everyone else does. That’s exactly what those ugly cost-allocation fights in Texas, Tennessee, and Oregon are about: regulators trying to reprice that standby product mid-game. Imagine if Kalshi could just change your contract price with two seconds left in Game 5 of Knicks–Spurs you’d scream it’s unfair. But the grid has no other option, the costs are real, and somebody has to recover them.

If the stack can flex or even export, we stop buying insurance from the grid and start selling it. Figuring out the last 5% is so exciting, it's the only slice of the stack nobody owns yet, and there will be real winners!

Other things I’m keeping an eye on this week:

China’s grid added 18 GW / 65 GWh of storage in a single month late last year. That’s a quarter of the entire global 2025 deployment in thirty days. Insane scale.

GM’s Ultium JV is spinning up LFP production for grid storage in July, with sodium prototype cells due by year-end. Using idled EV lines to absorb storage demand is smart.

Inlyte Energy is commissioning a 600 kWh iron-sodium pilot inside a Tier IV Swiss data center late this year. Need to check their data when it goes live.