🌿 Friday's Climate Infra Brief: Construction Autonomy

Happy 4th! Have you ever wondered why we can’t build faster?

You hear the usual answer: it’s a labor shortage. Construction needs 349,000 net new workers in 2026 just to backfill retirements. The most skilled people on any jobsite who can run an excavator or a dozer blade to grade are usually the oldest on site, who are retiring. The apprenticeship pipelines are thin, and 1/4 of the workforce is foreign-born at a moment when construction firms say immigration enforcement has already touched their projects. Besides the shrinking workforce, from 2000 to 2022, US construction labor productivity increased 0.4% per year on average. That is a cumulative 10% gain over two whole decades. For context, over that exact same period, manufacturing jumped 90%. Construction remains the one massive sector of our economy that never industrialized (you know what I mean if you’ve ever renovated a home). And ironically, this is also the very sector we are now begging to build out more infrastructure, data centers, power and grid assets, and fabs at a pace we’ve never seen before. Data-center construction is running at a ~$50B annual pace, up 28% YoY, and utilities have a $1.4T capital plan through 2030. Those projects are enormous, flat, repetitive scopes. The same task, thousands of times, against a deadline someone is losing a lot of money on is the best demand profile autonomy could ask for.

So where are we today with construction automation tech? Not a historian, but when I dug in, I was surprised to learn mining adopted autonomous haul trucks 20 years ago, driven by a similar labor shortage?! For construction, the most repetitive, highest-hours parts of any build are earthwork, grading, hauling, site prep. The math is closing today: the tasks repeat, output is measurable in cubic yards, machines can run hours no human shift allows, and one operator can supervise several units at once. The ROI is there, the demand is there. The foundational models that support the bottom of the tech stack are getting better, and robotics/physical AI is one of the hottest investment themes these days, so the capital needed to attract talent is also there. Stars seem to be aligning for companies in this space to change how we build.

Part 1 - The business model.

First: are you retrofitting or purpose-built? The retrofit players bolt autonomy onto machines contractors already own. Teleo built supervised autonomy where one remote operator runs multiple machines, any make, any vintage. SafeAI (acquired by ProntoAI in July 2025) does full-autonomy retrofits with safety-certified software and deployed with partners like Obayashi. Bedrock Robotics raised a $270M Series B with an ex-Waymo team for a kit that makes an existing excavator autonomous in hours. The appeal is obvious. You tap into a massive installed base, get to market fast, and ask the contractor for almost no upfront capex. Purpose-built machines should eventually win on unit economics and long-term reliability. Design out the cab, integrate the sensors, go electric. But you carry hardware capex and you’re competing with the incumbents’ dealer networks, which is a tough place to be.

And the incumbents stepped up this year. Caterpillar launched its construction autonomy line in January: autonomous excavators, loaders, haul trucks, the works. If the OEMs successfully embed autonomy at the factory, the window for anyone who is just a software play gets narrow fast. But that also makes these companies in this camp attractive acquisition targets. Teleo was reportedly acquired in February. The compelling position, I think, is building a great autonomous solution as a brand-agnostic layer across a mixed fleet.

The second fork: are you selling robots, or selling work? Selling machines is a hardware business with channel dependency, but it’s simpler. Selling work, robots-as-a-service or straight per-cubic-yard pricing, is a much better product for a contractor who wants certainty in cost cap. But it turns the autonomy company into a fleet owner and operator. And now you have a financing problem that anyone who has watched climate hardware scale will recognize immediately: capital assets with no operating history, no established residual value curves, and offtake that’s project-based instead of contracted. Banks pass on all three. What maybe available is warehouse credit lines, asset-backed facilities, and eventually securitization once the fleets mature. That credit market barely exists today. The equity market is charged though; construction robotics took $1.36B in the first three quarters of 2025, up 125% on all of 2024. If the ultimate product is autonomous work rather than autonomous machines, someone has to own and finance fleets of assets that will get deployed into concentrated demand. I feel the equity for that story has arrived, but the full capital structure hasn’t been built. My personal view: private credit should step up and do the interesting work to capture that spread.

There’s a nice wrinkle too: the machine’s own telemetry, hours and cycles and yards moved, is the underwritable data. The asset reports its own performance in real time, accurately. Rooftop solar never did that for its lenders.

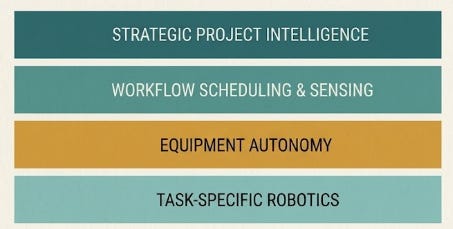

Part 2 - The tech stack (super high level).

Point robots, also called task robots. These are the machines that do one specific task incredibly well. Take Dusty Robotics. They print floor layouts at 40k to 70k sqft a shift for about $8k to $12k a month. A human crew is able to do 8k to 15k sqft. You also have Canvas hanging drywall and Hilti’s Jaibot handling overhead drilling. Civ is automating site survey and layout stakes. They are genuinely useful tools. But financially, they usually sell like hardware-plus-a-subscription, and venture rounds in this bucket only average ~$27M because it is niche. It’s tough to build a massive position there.

Autonomous heavy equipment. Bedrock Robotics’s got an ex-Waymo team building a system that can mount to an existing excavator in hours. Gravis is doing the same. Built Robotics is doing autonomous pile-driving. They have been serving solar farms, where the work is endlessly repetitive and the sites are totally empty. Planted Solar is another one. When real, heavy capital assets produce contracted, measurable usage, it is moving closer to the “new real asset” category.

Sensing and scheduling. This is huge. We’re talking autonomous scanners walking sites for QA, drone capture, and generative scheduling software. We are finally getting actual-versus-plan execution data, every single day, on every machine, and across the job site. Construction never had this. Look at ALICE Technologies. They take a BIM model and a P6 schedule, simulate millions of execution paths, and claim ~17% schedule compression alongside ~14% labor savings. Unlimited Industries is building an operating system for managing the execution. This category covers a very broad problem set that merits modern solutions: for example, paying a service to photograph and scan your jobsite on a fixed schedule costs maybe $4k to $5k a month. But construction often involves disputes, who broke what, what was behind that wall, whose delay was it, and a timestamped visual record ends those fights before the lawyers do. That’s credited with $80k to $150k of avoided claims per project. It sounds boring. Trust me, that’s a massive compliment.

Project intelligence. The build itself becomes priceable. Cost and completion assumptions are always the biggest source of variance in any project model. They are systematically optimistic (the joke we make is P90 means at 90% of the time our budget and schedule estimates are wrong). But if you compress that variance using hard data, everything downstream reprices. You get more leverage, lighter completion guarantees, cheaper surety bonds, and maybe even parametric cover that pays out on objective schedule triggers. A new crop of companies is already racing to own this pricing layer. Take Build, a New York startup. They just raised an $8.5M seed led by Index Ventures to automate data-center site sourcing and technical due diligence. They sell it as a service rather than software. Occam Edge over in San Francisco works the exact same seam but from the risk side. They translate execution and technology risk into strict bankability terms that investors can actually act on. Their data-center work pegs each GW-month of delay at a staggering $0.7–0.9B in deferred revenue, and they found that the best predictor of on-time delivery is permitting readiness.

PS: If you enjoyed this, share it with a colleague or friend who might too. And if you want to chat, I’m at meng@fridaymorninglabs.com

Sources: Associated Builders and Contractors 2026 workforce forecast; AGC/Sage 2026 Construction Outlook; US Census Bureau Construction Put-in-Place; Caterpillar, "Next Era of Autonomy in Construction" (Jan 2026); Equipment World and trade reporting on the Heidelberg Materials/Pronto mixed-fleet quarry trial; PitchBook (Teleo acquisition, Feb 2026); company disclosures (Teleo, SafeAI, Bedrock Robotics, Built Robotics); Zacua Ventures / Hilti Ventures / 94 Ventures Construction Robotics Report 2026; Index Ventures and Tech Funding News on Build's seed; Occam Edge, "Confronting the Datacenter Delay Dilemma." Figures as of early–mid 2026.